Long-term political agreements over ad hoc policy

A recent Mises Daily article by Frank Shostak at Mises.org covers the road Estonia has taken since the economic bubble burst a few years back. The core statement in the piece is how a non-inflationary monetary policy and the lack of government bailouts can cure the economy from the structural illnesses that grow out of an inflationary boom. As the author points out, this is precisely the reason why Estonia has fared so well compared to the rest of the Europe.

But while he argues that the success came thanks to the decisions made by the current government I make the case for a different approach. Instead, I claim that Estonia is a good example of why a democratic system must be guided by firm economic principles rather than be suitable for ad hoc policies.

Shostak writes that Estonian GDP and labor market have improved significantly since the crash and that we are strongly outperforming the general trend in the EU. There is no denying that Estonian economy, being lead by international trade has recovered well over the last two years. And although there is still a bit to go before reaching the peak levels of 2007 the consensus among local analysts is that the underlying structure of the economy is far healthier now.

As for the unemployment, the recovery has been as strong. Even though Shostak’s data underestimates the current levels, the trend is represented accurately. It is also noteworthy that even during the height of the preceding boom the unemployment fell barely below 5%. In this light the 10,2% today seems a fairly good number in comparison to western countries that are used to even lower natural levels.

Source: Statistics Estonia

Now, for the tricky part. Despite Shostak being right about the fall in money supply and government spending during the crisis, he unfortunately misses on the reasons for that and therefore also comes to wrong conclusions in regard to the actions of the government.

Rather than persisting with the cleansing process, the government and the central bank have chosen to reverse the stance, thereby arresting the process of healing the economy.

This is always the danger when basing your analysis simply on data without deeper knowledge of the specifics in a given system.

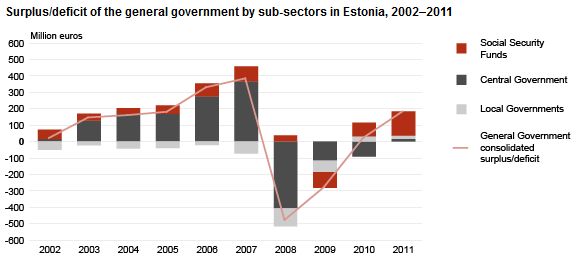

The secret of the Estonian success lies actually in the political traditions started 20 years ago, right after the Soviet Union fell apart. Ever since becoming independent all ruling coalitions have adopted the principle of a balanced budget. So, in essence the government has not been able to spend more than its incomes. As a result a fall in the GDP and therefore in tax revenue necessitates less spending while a growing economy enables more spending. Occasionally there has been even talk of adding this principle to the constitution.

Another reason that has held public spending in check has been the long-term policy of integration with European Union which during the crisis brought us on the brink of joining the Euro area and therefore required the fulfillment of the Maastricht criteria of low public deficit.

Source: Statistics Estonia

The Estonian Central Bank has similarly had its hands tied. The reason being that the local currency was set up on the basis of a currency board. This was achieved by pegging the Estonian Kroon to the German Mark (later switched for the Euro), the entire money supply had to be backed by foreign currency or gold. In addition, the ability to change this monetary setup was given solely to the parliament, while the central bank was also forbidden to give out loans to central and local governments. As a consequence the ability of the central bank to manipulate the money supply became very limited. The only available tool left was the reserve ratio of commercial banks, which before the acceptance into the Euro area was at 15%. Afterwards it was gradually dropped to the ECB levels.

Knowing all this we can understand how the contraction in the spending of the Estonian government was caused by the traditions of fiscal policy while the changes in the monetary base were brought about by banks buying local currency in exchange for foreign ones. Both processes are also represented in Shostak’s graphs. While the boom driven by loose monetary policy abroad helped to fuel one in Estonia as well, the following recession has helped to clean up the economy as the government has lacked the ability to go down the road of bailouts and stimuluses. Principles set in place two decades ago also provided the government with good excuses against public pressure favoring intervention.

But Estonia presents us with another related interesting insight. The limitations set upon the public sector create a situation where its welfare is directly dependent on how the private sector is doing. This helps to hold back the growth of government beyond sustainable levels. Perhaps we could even argue that it creates some incentives for politicians and bureaucrats to actually work in favor of the taxpayers. For example the main focus of the Estonian government during the crisis was to promote entrepreneurship and reform legislation accordingly.